The Fed held rates at 3.50%–3.75% yesterday, but that's not really the headline. The signal is what matters — another hike could come later this year. According to Reuters, the dot plot suggests officials expect borrowing costs to stay elevated through 2026. For construction project managers dealing with financing terms, material procurement, and milestone payments, that changes the calculus on basically everything.

General contractors right now are scrambling to restructure their financing packages. A mid-sized commercial contractor in Phoenix told me they're looking at an extra $280,000 in carrying costs on a $12 million office complex because their construction loan repriced last month. Their original budget assumed rates would drop by Q3. They're eating the difference.

This isn't just about higher interest payments. When construction project financing gets more expensive, the whole operational flow shifts. Payment schedules tighten. Procurement strategies change. Cash preservation becomes critical. And every delayed milestone suddenly costs a lot more than it used to.

The hidden squeeze on construction margins

Construction project financing works differently than most business loans. You're not borrowing a lump sum — you're drawing funds as you complete phases, paying interest on outstanding balances while racing to finish before rates move against you.

Take a typical $8 million multifamily project. With construction loans now pricing around 8.5% to 9.5% (up from roughly 6% eighteen months ago), every month of delay costs an extra $15,000 to $20,000 in interest alone. But the real damage comes from the compounding effects.

Material suppliers are tightening credit terms because their own financing costs went up. Where you might have gotten net-60 on structural steel last year, suppliers now want net-30 or COD on larger orders. That forces earlier draws from your construction loan, increasing your interest burden across the entire project.

Subcontractors face the same pressure. They can't float payroll for three weeks anymore, so they're pushing for faster payment or walking off sites. A foundation contractor in Dallas literally stopped work on day 22 of a net-30 payment term recently. The GC had to wire funds immediately, blowing up their entire draw schedule.

Procurement timing becomes a chess game

The standard approach to construction procurement — order when you need it — falls apart when rates stay high. Smart PMs are completely rethinking their purchasing strategies.

Keep your construction projects on schedule and budget.

Projbrick helps you plan, track, and manage every project phase with precision and ease.

- Real-time project tracking

- Resource & budget management

- Team collaboration tools

No credit card required

What's actually working: selective early procurement based on financing math, not just lead times. If you can lock in lumber prices now and store it for three months, the carrying cost might be less than the combined hit from price increases plus higher loan interest later.

They calculate total financing cost for every major material category:

-

Storage and insurance if bought early

-

Expected price movement over the project timeline

-

Interest differential between early and scheduled draws

-

Opportunity cost of tying up credit capacity

Negotiate early payment discounts and confirm return policies before buying long-lead items.

For their current project, buying mechanical equipment four months early saves $42,000 versus waiting until installation phase. That math only works because they negotiated a 2.5% early payment discount with the supplier and have warehouse space left over from a previous job.

But this approach breaks down fast if you miscalculate. Another contractor tried the same thing with finish materials — bought $180,000 of tile and fixtures early to lock prices. Then the owner changed the design. Now they're paying 8.75% interest on materials sitting in storage while trying to return or resell half the inventory.

Milestone restructuring saves serious money

Traditional milestone structures assume steady cash flow and predictable financing costs. With rates elevated and volatile, those assumptions kill margins.

The old model: 10% deposit, 15% at foundation, 20% at framing, and so on. Simple, clean, expensive in this environment.

| Model | Milestones |

|---|---|

| Old model | 10% deposit, 15% at foundation, 20% at framing, and so on. |

| Restructured model | 25% upfront, 35% at 30% completion, then smaller draws through finish. |

A concrete contractor in Houston restructured all their commercial contracts to collect 25% upfront, 35% at 30% completion, then smaller draws through finish. It sounds aggressive, but the math supports it. By reducing their average outstanding loan balance by around $400,000 across the project timeline, they save roughly $2,800 per month in interest. Over a seven-month project, that's nearly $20,000 straight to the bottom line.

The key is making this palatable to owners who have their own financing pressures. A few things that actually get accepted:

Offer a small discount for accelerated payment — maybe 1.5% off the total contract. You'll recover it in reduced financing costs if your loan is priced above 7%.

Build in explicit rate escalators. If the Fed funds rate increases more than 50 basis points during the project, payment terms automatically adjust. Most owners understand this given current conditions.

Create optional early payment incentives. Give owners the choice to pay certain milestones early for a 2% discount. Some will take it if their cash position is strong, saving you carrying costs.

Cash flow forecasting with rate scenarios

Every construction PM runs cash flow projections. But most still use static interest rate assumptions, which at this point is like navigating with a pre-pandemic map.

Proper construction project financing analysis now requires multiple rate scenarios — not just "what if rates go up 1%" but specific, time-based models reflecting likely Fed action dates and loan repricing schedules.

A framework that actually helps:

Base scenario: Current rate environment holds through project completion. Calculate your total financing cost, payment timing, and margin impact.

Stress scenario: Rates increase 75 basis points at your next loan adjustment (usually quarterly for construction loans). Model how this affects each remaining draw and total project cost.

Opportunity scenario: Rates drop 50 basis points in six months. Seems unlikely given the Fed's statement, but worth modeling to decide whether to lock rates now or stay floating.

Run these for every major bid and active project. A mechanical contractor doing this exercise found that three of their five active projects would go negative margin if rates moved just 50 basis points more. They renegotiated payment terms on two of them and walked away from the third.

Contract language that protects against rate volatility

Standard construction contracts barely mention interest rates. AIA documents have some force majeure language, but nothing specific to financing cost changes.

Worth adding:

Rate adjustment clause: "If the Federal Reserve raises the federal funds rate by more than 0.75% cumulative from contract signing, contractor may request equitable adjustment to contract sum to offset increased financing costs."

Financing contingency: "This contract is contingent upon contractor securing construction financing at an interest rate not exceeding [X]%. If financing is unavailable at or below this rate, contractor may terminate without penalty within 30 days of contract execution."

Payment acceleration rights: "If prime rate exceeds [X]%, contractor may invoice for stored materials and completed work weekly rather than monthly, with payment due within 10 business days."

Most owners push back initially. But when you show the math — how rate increases could push you into default, threatening project completion — reasonable owners recognize it's better to share some risk than inherit a stalled project.

The automation advantage in volatile rate environments

When rates shift, you need to recalculate dozens of variables across multiple projects quickly. Manual spreadsheet updates can't keep pace with that.

AI-powered operational software changes how you handle rate volatility. Instead of updating static cash flow projections once a month, these platforms continuously recalculate financing costs based on current rates and flag projects where margins drop below a set threshold.

The better platforms connect your rate scenarios directly to procurement decisions. When the Fed signals higher rates ahead, the system can adjust recommended purchase timing for long-lead materials, calculating the balance between early procurement costs and future rate risk.

There's also a pattern-recognition value that only shows up when you're tracking everything systematically. A concrete contractor using one of these platforms noticed that projects with front-loaded payment structures stayed profitable even at 9% interest, while traditional milestone structures went negative at 8.25%. They restructured every new contract based on that finding, protecting a meaningful chunk of annual margin.

On the administrative side, when you need to request payment term modifications across fifteen active projects, AI automation can generate customized requests based on each contract's specific language and rate triggers — work that would otherwise take days.

Timing your loan locks and construction starts

The old approach was simple: lock your construction loan rate when you break ground. That made sense when rates moved gradually.

Now, with the Fed signaling potential hikes ahead, the calculation is more complicated. Lock too early and you're paying commitment fees on unused funds. Lock too late and you might face a 50-basis-point jump that wrecks your margin.

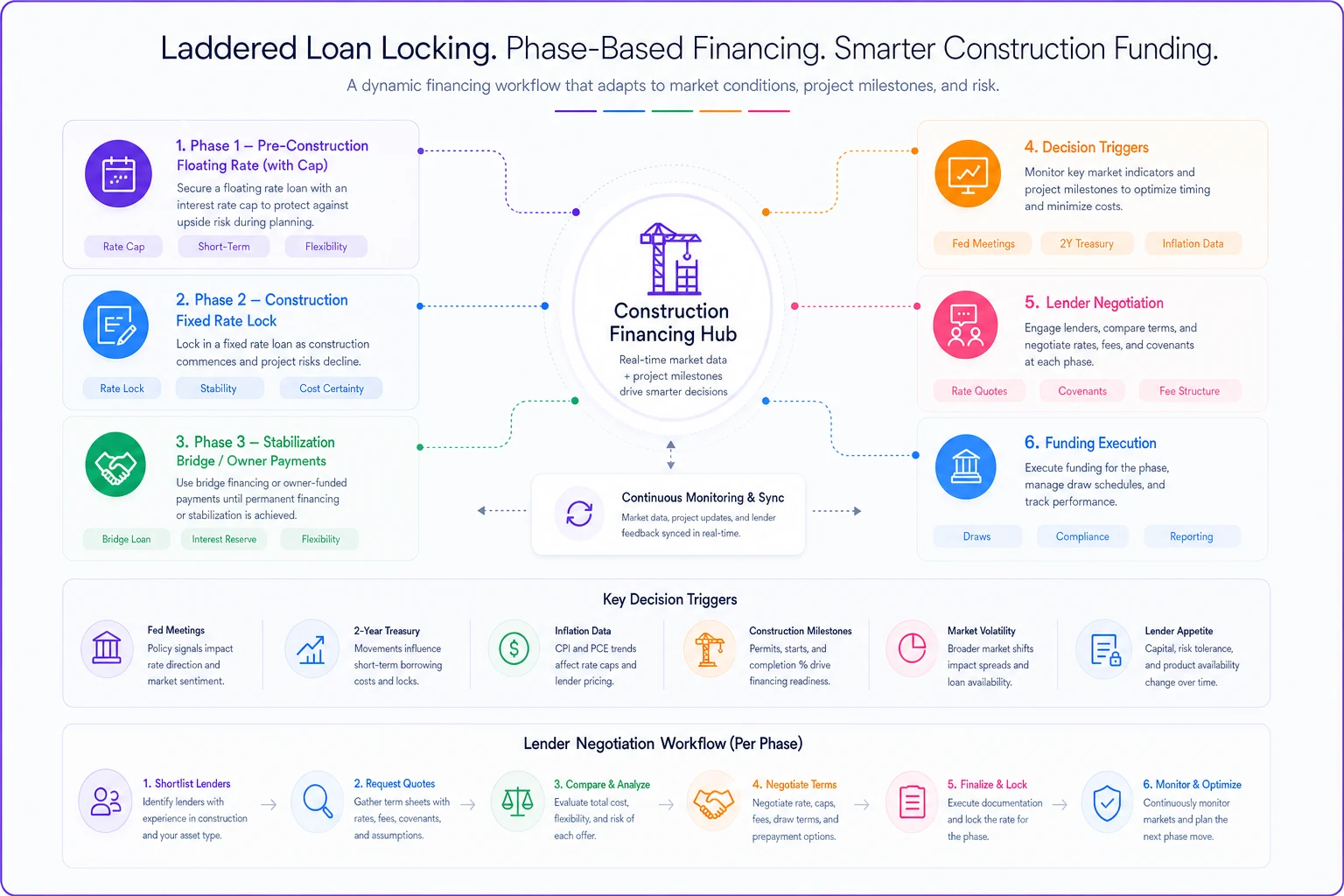

A laddered approach is working well for some contractors. Instead of one construction loan for the entire project, they break financing into phases:

Phase 1 (0–35% completion): Floating rate with a cap — some upside if rates drop, protection against major increases

Phase 2 (35–70% completion): Fixed rate locked 60 days before phase start, when Fed direction is clearer

Phase 3 (70–100% completion): Bridge financing or accelerated owner payments to minimize interest exposure during the highest-cost stretch

A visual workflow for laddered loan locks and phase triggers:

This takes more negotiation with lenders and more documentation. But on a $10 million project, proper rate timing can save $150,000 or more in total interest.

The trigger points matter too. Don't just watch Fed meetings — track the 2-year Treasury yield, which tends to predict Fed moves months in advance. When the 2-year starts climbing, construction loan rates usually follow within 45 to 60 days.

Restructuring existing projects before it's too late

If you have projects underway with floating-rate construction loans, waiting to see what happens is the expensive option. Even with the administrative hassle, restructuring now could save real money.

Start with projects that have the longest remaining duration. A project at 30% completion with nine months left carries far more rate risk than one that's 80% done.

For each vulnerable project, model three options:

Convert to fixed rate now — you accept current rates but eliminate future risk. Most lenders will do this for a fee, typically 0.5% to 1% of the outstanding balance.

Blend and extend with your lender — accept a slightly higher rate now in exchange for rate protection through completion, plus potentially better terms on your next project.

Refinance with a different lender if the savings justify the hassle. Construction loan transfer is messy but possible.

A Florida GC recently went through this on four active projects. Two they left floating (nearly complete), one they converted to fixed (18 months remaining), and one they refinanced with a credit union offering 125 basis points below their current rate.

Supplier financing alternatives

When traditional construction project financing gets expensive, some suppliers step in. These arrangements come with complications that contractors often don't fully think through.

Equipment suppliers increasingly offer lease-to-own structures that keep items off your construction loan. Monthly payments might look higher than interest-only draws, but the total cost could be lower when you factor in rate risk.

Material suppliers are getting creative too. One lumber supplier in Texas now offers a "price lock plus financing" arrangement — you commit to buying at today's prices, they hold the inventory and finance it at prime plus 2%, you draw materials as needed. It's essentially vendor-managed inventory with embedded financing.

The catch: these arrangements usually require personal guarantees or liens that go beyond normal trade credit. And if the supplier runs into financial trouble, your material supply and financing could disappear at the same time.

Moving forward with smart phase planning

This environment rewards contractors who treat construction project financing as part of operations, not just a necessary overhead. Every decision — phase sequencing, material procurement, crew scheduling — has financing implications that compound when rates stay elevated.

The contractors holding up right now share a few things in common. They model rate impacts before bidding, not after. They negotiate payment terms as hard as they negotiate scope. They treat financing costs as a line item to optimize.

They've also integrated their phase planning frameworks with their financing strategies. When every delayed milestone costs more in interest, preventing phase slippage becomes even more important. The same operational discipline that keeps projects on schedule also protects margins from rate-driven erosion.

Making immediate adjustments

Tomorrow morning, pull the financing details on every active project. Calculate what happens to each one if rates increase 50 basis points at your next adjustment date. For any project where that pushes margins below 5%, start restructuring conversations now.

Review every pending bid with fresh rate assumptions. That school renovation you priced assuming 7.5% construction loan rates may need to be repriced if your lender is now quoting 8.25%.

Economists surveyed by Reuters expect rates to hold this year, but the risk of another hike hasn't gone away. Construction project financing needs to be managed as deliberately as materials and manpower. The companies that get through this will be the ones that made adjustments before their margins were already gone.

Ready to build smarter and faster?

Join 2,000+ construction teams using Projbrick to improve project visibility, reduce delays, and increase profitability.